Dominican Republic Second Home Mortgage Rates Guide

Dreaming of a second home in the Caribbean can feel complex, but financing your slice of paradise in the Dominican Republic is more straightforward than you might think. As Las Terrenas’ leading real estate experts for over 25 years, we at Atlantique Sud have guided countless international buyers through this exact process. The key is understanding one simple fact: second home mortgage rates here are typically higher than for a primary residence in your home country.

This isn't a barrier; it's just business. Lenders view an international, non-primary property as a slightly higher risk. Grasping this distinction is the first step to confidently financing your dream villa or condo in Las Terrenas.

Financing Your Dream Home in the Dominican Republic

For over 25 years, our team at Atlantique Sud has helped North American and European investors navigate the unique financial landscape here in Las Terrenas. Success isn't about complexity; it’s about knowing what Dominican banks look for when lending to foreign nationals.

Unlike a mortgage in your home country, financing a vacation property here operates under different criteria. Your final terms will be shaped by local banking policies, your financial profile, and the specific property you intend to purchase.

Key Considerations for International Buyers

The path to securing financing is completely manageable once you know what to expect. Here are the main factors that will influence your experience:

- Higher Down Payment: Plan for a larger down payment, typically between 30% and 50%. This is how local banks mitigate risk and confirms you are a serious, committed buyer.

- Property Type Matters: Lenders view a pre-construction condo under the tax-incentivized CONFOTUR law very differently from a standalone resale villa. New developments often have established banking relationships, smoothing out the process.

- Documentation is Key: Be prepared with comprehensive paperwork. Lenders will require proof of income from your home country, international credit history, and details of the property you plan to purchase.

Why Las Terrenas Is a Smart Investment

The allure of the Samaná Peninsula is more than just stunning beaches; it's a robust market delivering real returns. Investors in Las Terrenas consistently see strong rental yields, often ranging from 5.6% to 7.7%, fueled by a thriving tourism sector and a growing expat community.

That strong rental income potential is a significant plus, not just for your portfolio, but for your lender as well. It demonstrates the property is a performing asset.

As the leading real estate authority in Las Terrenas, we've helped countless clients structure their finances to acquire properties that are not just beautiful retreats but also powerful assets. Our deep relationships with local financial institutions are your direct advantage.

This guide is your roadmap. We’ll break down exactly how second home mortgage rates are determined, what you can do to secure the best terms, and how to turn your dream into a reality. With the right expertise and a local partner, the path to ownership is clear. Contact our team at Atlantique Sud to start your personalized property journey today.

Why Second Home Mortgages Are Different Here

So, why does a lender in the Dominican Republic view a second home mortgage differently? Understanding their perspective is the first step to securing great terms. For a bank, your primary mortgage back home is their safest bet. When financing a second home in Las Terrenas, especially for a non-resident, they see it as a higher-risk proposition.

This shift in perspective is precisely why second home mortgage rates and requirements are different. It’s not a roadblock; it's simply how lenders calculate business risk. At Atlantique Sud, our role is to demystify this process, so you can enter negotiations with confidence.

The Lender’s Point of View

From a lender's perspective, a second home is a "want," not a "need." This distinction colors their entire risk assessment. If a borrower faces financial hardship, they will prioritize protecting their primary family home. Payments on a vacation property are often the first to be missed.

This is a universal banking principle, but it's amplified when dealing with international clients. The legal process for cross-border recourse is complex and costly for a bank. To mitigate this risk, they build safeguards into their mortgage terms.

Lenders aren’t just financing a property; they are assessing a commitment. A second home mortgage for an international buyer is seen as a higher-risk loan, which naturally leads to different lending criteria compared to a primary residence loan.

This higher perceived risk translates directly into the offer you receive. Dominican banks will adjust their requirements accordingly, which usually means:

- Higher Interest Rates: The rate for a second home will almost always be higher than for a primary one. This is how they price in the additional risk.

- Larger Down Payments: Expect to put down between 30% and 50%. This lowers the bank's exposure and demonstrates your financial commitment.

- Stricter Income Verification: They will thoroughly review your proof of income and overall financial health to ensure you can comfortably manage another mortgage.

From Risk to Opportunity

While the bank focuses on risk, a savvy investor sees an opportunity. By understanding what makes lenders cautious, you can build an application that addresses their concerns directly. A larger down payment, for example, is a powerful bargaining chip that can lead to better second home mortgage rates.

The local market is also a crucial factor. A property in a prime neighborhood like Playa Bonita or a new build in Cosón has excellent rental potential, with yields often between 5.6% and 7.7%. Presenting solid rental income projections helps the lender see the property as a performing asset, not just a personal expense.

This is where our 25+ years of experience in the Las Terrenas market at Atlantique Sud becomes invaluable. We help you build a compelling case for the bank because we know precisely what they need to see. By preparing for these expectations, you'll find the process much smoother.

Key Factors That Shape Your Mortgage Rate

When a Dominican bank reviews your mortgage application, they are assembling a financial puzzle to determine their risk, which ultimately sets your second home mortgage rates. Understanding each piece puts you in a stronger position to secure the best possible terms for your new home in Las Terrenas.

At Atlantique Sud, we guide our clients through this every day. It's about knowing which levers to pull to present yourself as a low-risk borrower. Let's break down what Dominican lenders focus on.

Your Financial Profile and Credit History

Your financial health is the foundation of your mortgage application. Lenders need to see a stable, reliable income that can easily support your current obligations plus this new mortgage. But what about your credit score from your home country?

While a Dominican bank can't pull your FICO or European credit report directly, your creditworthiness is still paramount. You will be asked to provide letters of good standing from your current banks and documents proving a history of responsible borrowing. Understanding what is a credit score and why it matters is a smart first step.

The Power of the Down Payment and LTV

In the Dominican Republic, your down payment is your single most powerful negotiating tool. Lenders typically expect foreign buyers to put down between 30% and 50% of the property’s value.

This upfront cash significantly lowers the bank's risk. The key metric they use is the Loan-to-Value (LTV) ratio—the percentage of the property's price covered by the loan. A 40% down payment results in a 60% LTV.

A lower LTV is the clearest signal you can send to a lender that you are a low-risk, financially secure buyer. This single factor can have the biggest impact on lowering your final interest rate.

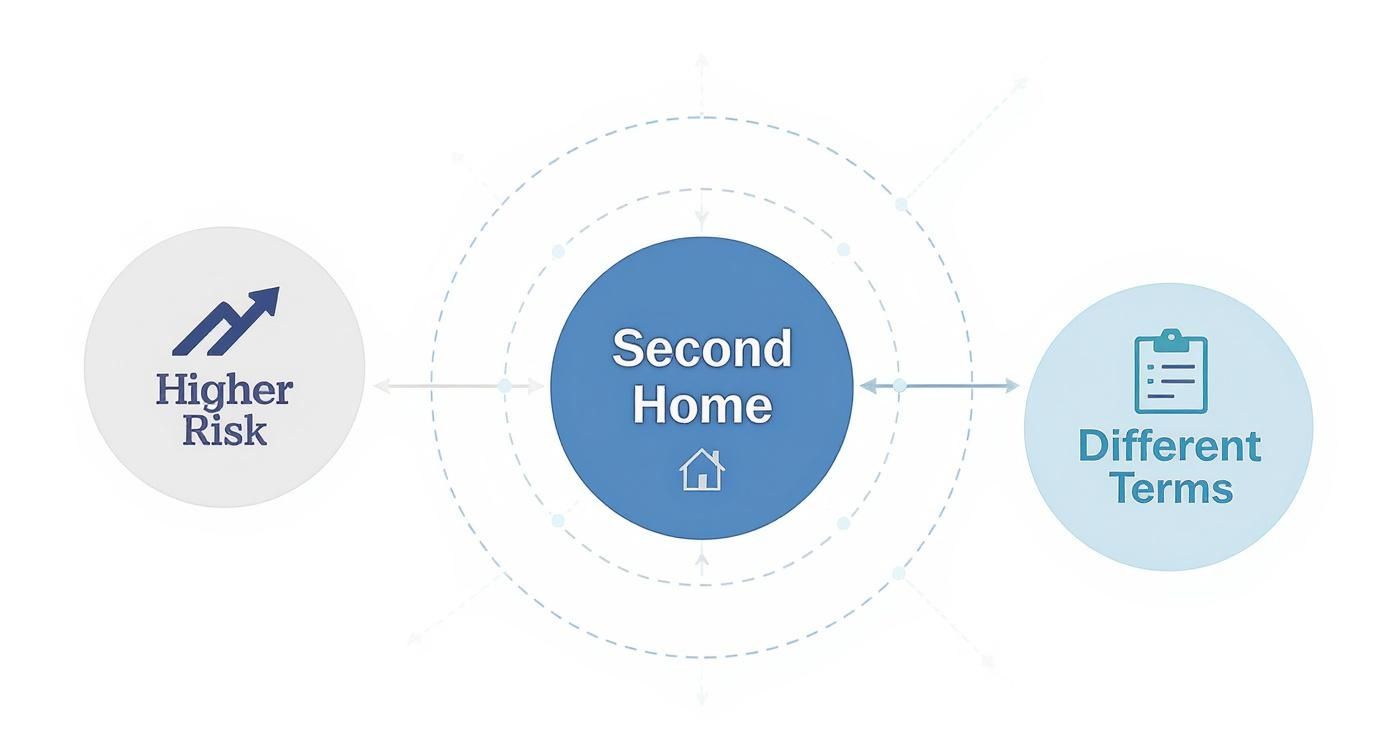

The infographic below illustrates how lenders view a second home loan and why the terms differ from a primary mortgage.

As you can see, the bank’s perception of higher risk drives the tougher lending terms. A substantial down payment is critical because it immediately calms those concerns and proves you have significant skin in the game.

How Your Profile Impacts Your Second Home Mortgage Rate

This table shows how key factors can influence the interest rate you're offered for a second home in the Dominican Republic.

| Factor | Favourable for Lower Rate | Leads to Higher Rate | Atlantique Sud's Expert Tip |

|---|---|---|---|

| Down Payment | 40% or higher | Below 30% | This is your strongest card. Maximize your down payment to show financial strength and reduce the lender’s risk. |

| Credit History | Verified history of on-time payments, letters of good standing | Limited credit history, past defaults | Prepare a file with letters from your banks and proof of responsible borrowing. It makes a huge difference. |

| Property Type | New construction, condo in a managed development | Older, standalone property in a remote location | Lenders love properties under the CONFOTUR law as they've already been vetted and signal a secure investment. |

| Loan Term | 15 or 20 years | 30 years | A shorter term means less long-term risk for the bank, often resulting in a better rate for you. |

Being strategic about these factors can save you a significant amount over the life of your loan. You have more control over the outcome than you might think.

Property Type and Location Specifics

Not all properties are equal in a lender's eyes. The type of home and its location directly affect your mortgage rate. A pre-construction condo in a new development in Playa Popy is often seen as lower risk than an older, standalone villa in a more remote area.

Properties under the CONFOTUR law are especially appealing to lenders. These projects have government approval, offer tax incentives, and signify a stable, high-demand investment. Our local knowledge is your advantage; we guide you toward properties that are not only beautiful but also financially smart.

Loan Term and Currency Selection

The loan structure also plays a role. Shorter loan terms—15 or 20 years instead of 30—usually come with lower interest rates because the bank recovers its capital faster, reducing long-term risk.

You will likely have the choice between loans in Dominican Pesos (DOP) or U.S. Dollars (USD). Most of our international clients opt for USD loans. This eliminates currency fluctuation risk, especially if your income and rental revenue are also in USD, creating a stable and predictable financial picture.

Your Step-by-Step Guide to the Mortgage Application Process

Obtaining a mortgage in the Dominican Republic as a foreign buyer is a straightforward journey with an expert local partner. While the paperwork may differ from your home country, the process is clear and manageable.

At Atlantique Sud, we make this process feel effortless. We connect our clients with the best local banks, bilingual attorneys, and notaries, ensuring a secure and transparent transaction. Think of us as your boots on the ground, handling every detail professionally.

Phase 1: Pre-Approval and Documentation

Your first step, even before you find the perfect villa, should be getting pre-approved. A pre-approval from a Dominican bank establishes your budget, shows sellers you're a serious buyer, and strengthens your negotiating position.

To begin, you'll need to gather your financial documents. This is the most critical part of the application, as it provides a complete picture of your financial health.

Your documentation package will generally include:

- Valid Identification: A clear copy of your passport and a second photo ID.

- Proof of Income: Recent pay stubs, an employer letter, or tax returns from the last two years from your home country.

- International Bank Statements: The last three to six months of statements from your main bank accounts to verify assets.

- Credit History: A letter of good standing from your current bank and other documents demonstrating responsible borrowing.

- Property Information: Once selected, you'll need the signed Promise of Sale agreement and a copy of the property title (Certificado de Título).

Phase 2: Underwriting and Property Valuation

After submission, your file enters underwriting. The bank's analysts review your paperwork to assess risk and determine your final second home mortgage rates. This typically takes a few weeks, and requests for additional information are common.

Simultaneously, the lender orders an official property appraisal. A certified appraiser determines the home's current market value. This is crucial, as the bank will only lend a percentage of this appraised value (the LTV ratio).

From submitting a complete application to receiving the keys, the entire process typically takes 30 to 60 days. Having a team like Atlantique Sud in your corner helps avoid common delays by ensuring your file is perfect from day one.

Phase 3: Closing the Deal

Once the bank approves your loan, it's time to close. Our network of trusted local attorneys will conduct final due diligence, confirm the property title is clean, and prepare all closing documents.

The final step is signing the mortgage agreement at a notary's office and transferring funds. Our team coordinates everything between the bank, the seller, and your lawyer to ensure a smooth, timely closing, handling any language or legal barriers along the way.

For a broader view of your options, explore our guide on financing real estate in the Dominican Republic, which covers mortgages, loans, and alternatives.

Alternative Financing Strategies to Secure Your Property

While a traditional Dominican bank mortgage is a common route, it’s not the only way to finance your Caribbean dream. Over our 25+ years in Las Terrenas, we've helped savvy international clients use creative financing that offers more flexibility, speed, and sometimes better terms than a standard loan.

Exploring these alternatives can be a game-changer, especially in a competitive market. These routes allow you to move quickly and negotiate from a position of strength, whether you're eyeing a new condo or a resale villa.

Developer Financing For New Construction

One of the most popular alternatives, especially for pre-construction, is developer financing. The teams behind new communities in Las Terrenas often offer their own financing packages directly to buyers. For international investors, this can be transformative.

The qualification process is usually simpler and faster than a bank's. Motivated to sell their properties, developers often provide competitive rates and flexible payment plans tied to construction milestones.

For new builds, developer financing streamlines the entire purchase. It removes many of the hurdles of a conventional bank loan, creating a direct and often more efficient path to ownership for our foreign clients.

This option is particularly attractive for properties under the CONFOTUR law, as the project has already been vetted. It’s a straightforward way to secure a brand-new asset with built-in financial advantages.

Seller Financing: An Agreement With The Owner

Another powerful strategy is seller financing. In this arrangement, the property owner acts as the lender. You provide a deposit and pay the remaining balance in instalments over an agreed-upon term, with interest.

This setup offers incredible flexibility, as the interest rate, payment schedule, and loan term are all negotiable. It’s a fantastic option for unique properties that might not fit a traditional lender’s rigid criteria. For a deeper look, our guide covers everything you need to know about second home down payment requirements.

Using Home Equity From Your Primary Residence

For many buyers from North America or Europe, the most potent strategy is tapping into the equity of their primary residence. A Home Equity Line of Credit (HELOC) or home equity loan can unlock the capital for a cash offer in Las Terrenas.

This approach instantly makes you a cash buyer, dramatically strengthening your negotiating position. Cash offers are appealing to sellers because they are faster, simpler, and less risky, often leading to a better purchase price and a seamless closing.

- Increased Negotiating Power: Sellers almost always prioritize cash offers, giving you a serious competitive edge.

- Faster Closing Times: Without waiting on bank underwriting, you can close the deal in a fraction of the time.

- Simplified Process: You handle financing in your home country, keeping the Dominican Republic transaction clean and straightforward.

To maximize your investment, it’s wise to explore top real estate investment tax strategies. At Atlantique Sud, we present this full range of solutions to find the one that best fits your personal goals.

Partner With Las Terrenas Real Estate Experts

Navigating second home mortgage rates in another country can seem daunting, but it's entirely manageable with the right team on the ground. In the Dominican Republic, securing financing is about working with experts who have spent decades building the right relationships and understanding the local system.

That's where we come in. For over 25 years, Atlantique Sud has been the trusted partner for North American and European buyers making Las Terrenas their home. Our long-standing connections with reputable local banks mean we can connect you with lenders who understand and welcome international buyers.

Your Direct Advantage in Las Terrenas

We are more than real estate agents; we are your strategic advisors. We translate your dream of a Caribbean home into a solid, actionable plan, having guided hundreds of clients through this exact process. We help them secure properties that become both cherished retreats and smart investments.

Our proven track record turns a potentially complex international purchase into a smooth, straightforward success. From pre-qualification to coordinating with bilingual attorneys, our comprehensive approach provides total confidence and clarity.

Let our experience be your advantage. We bridge the gap between your financial world back home and the incredible opportunities waiting for you in the Dominican Republic.

Take the Next Step Towards Ownership

The most important step is the first one: a personalized consultation with our team. We'll discuss your financial goals, review your investment profile, and introduce you to our network of trusted local lenders. From there, we’ll build a clear roadmap to securing your piece of paradise in Las Terrenas.

This is more than a transaction—it's a smart investment in your future. Our deep, firsthand knowledge of the Samaná Peninsula, combined with our financial expertise, puts you in the perfect position to succeed.

Don't let financing questions stop you from owning a home in one of the Caribbean's most stunning destinations. Contact Atlantique Sud today for a personal consultation, and let us show you just how achievable owning property in the Dominican Republic can be.

Common Questions About Dominican Republic Mortgages

Navigating the financial side of an international property purchase always raises questions. Drawing on our 25+ years of experience in Las Terrenas, we’ve compiled clear answers to the most common queries we hear from international buyers.

What’s a Typical Down Payment for a Foreigner in Las Terrenas?

For foreign buyers, Dominican banks typically require a down payment between 30% and 50% of the property's purchase price. A larger down payment strengthens your application and can help you secure more favorable second home mortgage rates by significantly reducing the lender's risk.

Are Mortgage Rates Fixed or Variable Here?

Both fixed and variable rate mortgages are available, though they may differ from what you're used to. It's common to find loans with a fixed rate for an initial period—often one to five years—before transitioning to a variable rate. Our team at Atlantique Sud leverages our banking relationships to find terms that align with your financial strategy.

Expert Tip: Getting pre-approved is a game-changer. A pre-approval from a Dominican bank gives you a solid budget to work with and makes your offer look much more serious when you find that perfect villa or condo. We can walk you through this process with our trusted banking partners.

How Long Does the Mortgage Approval Process Take?

With all your documentation in order, the timeline from application to final approval typically ranges from 30 to 60 days. Working with an experienced team like ours is key to preventing unnecessary delays and ensuring your property purchase proceeds smoothly.

Your dream home in Las Terrenas is closer than you think. The next step is a personal consultation to create a clear, actionable plan for your investment.

Contact Atlantique Sud Real Estate today, and let's put our 25+ years of local expertise to work for you.