Your Guide to Second Home Down Payment Requirements in Las Terrenas

Dreaming of a Caribbean retreat? The first question our international clients always ask is: “What are the real second home down payment requirements in Las Terrenas?” With over 25 years of experience guiding investors in the Dominican Republic, we at Atlantique Sud can tell you the answer is more accessible than you think. For most foreign buyers, the down payment ranges from 20% to 50%, depending on the property and financing structure.

Understanding Your Down Payment in Las Terrenas

Purchasing a second home in the Dominican Republic is an exciting milestone. Understanding the initial cash requirement is the first step toward making that dream a reality on the beautiful Samaná Peninsula.

Unlike a primary residence, lenders view a vacation property as a higher risk, which is why down payment requirements are typically higher. This is standard practice globally, and with our expert guidance, it’s a straightforward process to navigate.

At Atlantique Sud, our role is to demystify the process for our North American and European clients. We translate complex financial steps into a clear, actionable plan, ensuring you start your investment journey with absolute confidence.

Typical Down Payment Scenarios in Las Terrenas

So, what does that 20% to 50% range actually look like? It varies based on your choice of property. A pre-construction condo, for instance, follows a different payment schedule than a move-in-ready luxury villa.

To give you a clearer picture, here’s a snapshot of the Las Terrenas market—a market not only known for its beauty but also for delivering strong rental yields between 5.6% and 7.7%.

This table offers a quick overview of down payment expectations for different property types in Las Terrenas, showcasing the range of investment opportunities available.

| Property Type | Average Price Range (USD) | Typical Down Payment % | Estimated Down Payment (USD) |

|---|---|---|---|

| Pre-Construction Condo | $250,000 – $450,000 | 20% – 30% | $50,000 – $135,000 |

| Beachfront Apartment | $350,000 – $700,000 | 25% – 40% | $87,500 – $280,000 |

| Luxury Villa | $800,000 – $2,000,000+ | 30% – 50% | $240,000 – $1,000,000+ |

| Land for Construction | $100,000 – $500,000 | 40% – 50% | $40,000 – $250,000 |

The opportunities are incredibly diverse, from accessible and modern condos for sale in Las Terrenas to sprawling private estates. With our deep knowledge of the local market, we match you with an investment that fits both your financial goals and your vision for life in paradise.

Why Second Home Down Payments Are Different

Ever wondered why securing a mortgage for a vacation home feels different than buying your primary residence? It all comes down to how lenders, both in the Dominican Republic and abroad, perceive risk.

A second home is considered a discretionary asset—a luxury, not a necessity. If a homeowner faces financial difficulty, they will always prioritize their primary residence over a vacation property. This logic leads lenders to classify second home loans as higher risk.

This isn’t a barrier; it’s a standard practice in global real estate. Understanding this perspective is the first step to confidently navigating the second home down payment requirements and setting yourself up for a successful purchase in Las Terrenas.

Primary Residence vs. Second Home Risk

To balance this added risk, lenders require a larger down payment. By putting more of your own capital into the deal upfront, you demonstrate significant “skin in the game,” which lowers their potential loss.

Think of it this way: your down payment is a direct signal of your commitment. A bigger initial investment tells lenders you’re a serious, financially stable buyer, making you a much more appealing candidate for a loan.

This is why the typical down payment for a second home often starts at 10% to 20% for well-qualified buyers and can be higher depending on your financial profile. The more you put down, the stronger your application.

The Investor Angle Matters

When buying in a world-class destination like Las Terrenas, lenders recognize the property’s investment potential. They know these homes can generate fantastic rental income, with average yields often falling between 5.6% and 7.7%.

However, if you plan to rent it out for most of the year, your purchase may be classified as a pure investment property. This often comes with stricter down payment rules, sometimes requiring 25% or more.

Distinguishing between a second home and an investment property is a critical first step. Our team at Atlantique Sud has spent over two decades helping clients structure their purchases correctly. Read about the 7 reasons to choose Atlantique Sud to understand how our expertise ensures you get the best possible terms for your dream home on the Samaná Peninsula.

What Shapes Your Down Payment Amount?

When you’re buying a second home in the Dominican Republic, the down payment isn’t a one-size-fits-all number. It’s a dynamic figure influenced by a few key variables. As your trusted partners in Las Terrenas, we help you make sense of these factors to secure the best financing for your new property.

The process begins with your financial profile. Lenders will examine your credit score, existing debts, and income stability. A strong financial foundation reduces their risk, often resulting in more flexible down payment options.

The property itself also plays a massive role. For example, purchasing a pre-construction condo in a new development like those in the sought-after Playa Bonita neighborhood often comes with structured payment plans directly from the developer. This is entirely different from buying a resale luxury villa, which typically requires a larger, more traditional down payment upfront.

Your Finances and Property Choice

Lenders use a metric called the loan-to-value (LTV) ratio to determine how much they’re willing to lend. A higher down payment lowers the LTV ratio, making the loan less risky for the bank and your application much stronger.

To give you a real-world example, consider high-value markets. In a place like California, the minimum down payment for a second home might technically start low, but market realities often demand more. The average down payment for all buyers is around 13%, but putting down 20% is standard to avoid extra insurance costs. You can read more about these market dynamics to see how property values impact down payment expectations.

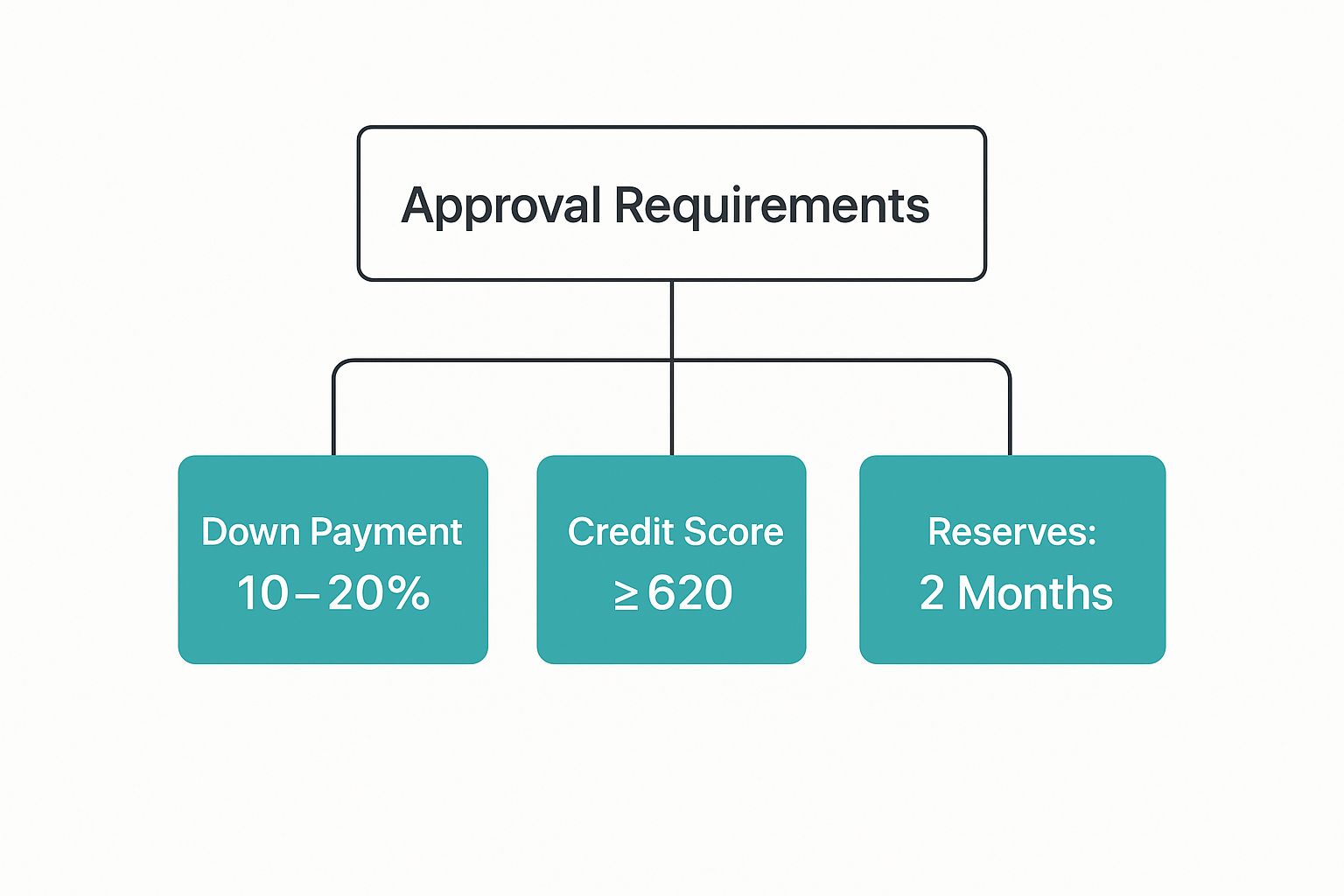

This infographic breaks down the core elements lenders evaluate when assessing a second-home buyer.

As you can see, it’s not just about the down payment. Lenders are also laser-focused on your creditworthiness and whether you have the cash flow to comfortably cover the expenses for both of your properties.

The Key Variables That Move the Needle

Ultimately, your down payment is a blend of lender requirements and your personal financial strategy. Here are the main elements we help our clients navigate:

- Credit Score: A strong score, typically 720 or higher, is your ticket to the lowest possible down payment options and the best interest rates.

- Property Type and Use: The requirements for a condo for personal getaways will differ from those for a villa intended as a full-time rental investment.

- Loan-to-Value (LTV) Ratio: This is the percentage of the property’s value you’re financing. A larger down payment means a lower LTV and better loan terms.

- Cash Reserves: Lenders need to see you have enough liquid cash to cover several months of mortgage payments for both your homes after the purchase closes.

At Atlantique Sud, we bring our 25+ years of experience to the table to guide you through each of these factors. Our goal is to ensure you present the strongest possible application to secure your dream home in Las Terrenas. Explore our exclusive villas for sale to see what’s waiting for you.

How to Finance Your Property in the Dominican Republic

Navigating financing in a new country can seem daunting, but the path to owning property in Las Terrenas is clearer than you might think. As your local guide, Atlantique Sud has spent over 25+ years building relationships with the most reliable financing sources for foreign buyers.

The good news is that the options are flexible. You are not limited to a single path but can choose the strategy that best fits your financial situation and the specific property you desire.

Common Financing Routes for Foreign Buyers

For international investors, three main avenues stand out when buying property in the Dominican Republic. Each has its own advantages, and understanding them is the first step to structuring a smart purchase.

- Developer Financing: This is a popular route, especially for pre-construction projects. Developers often offer payment plans tied to construction milestones, making it a straightforward and flexible option.

- Local Bank Mortgages: Obtaining a mortgage from a Dominican bank is a viable option for foreigners. While requirements may be stricter than developer financing, it opens up a wider range of properties, including resales. For details, see our guide on how to get a real estate loan from a Dominican bank.

- Leveraging Home Equity: Many of our North American and European clients use equity from their primary home via a HELOC or cash-out refinance. This allows them to make an all-cash offer in the Dominican Republic, strengthening their negotiating position.

Strategic Financial Advantages

Beyond these direct financing methods, a powerful tool in the Dominican Republic can significantly impact your second home down payment requirements: the CONFOTUR law. This law provides major tax exemptions for qualified tourism projects.

By purchasing a CONFOTUR-approved property, you are exempt from the 3% property transfer tax and the 1% annual property tax (IPI) for up to 15 years. This isn’t just a small discount; it can free up thousands of dollars that would otherwise be tied up in taxes.

This saved capital can be used for a larger down payment, helping you secure a better property or cover furnishing costs. As you explore your options, it’s also helpful to get familiar with specific products like investment property loans, which are tailored for buying income-generating assets.

At Atlantique Sud, we specialize in identifying these strategic opportunities. Our deep knowledge of the local market ensures you make the smartest financial move. We connect you with our trusted network of local lenders, developers, and legal experts to make your Caribbean dream a reality.

Tapping into Local Perks Like CONFOTUR

The down payment often feels like the biggest hurdle when buying a second home. But in the Dominican Republic, a powerful local incentive can significantly reduce that burden: the CONFOTUR law. For savvy investors, it’s a true game-changer.

As the leading real estate authority in Las Terrenas for over 25 years, we at Atlantique Sud have mastered these local advantages for our clients. The CONFOTUR law, designed to boost tourism development, offers massive tax breaks on certified properties.

How CONFOTUR Directly Boosts Your Buying Power

When you purchase a CONFOTUR-approved property, the benefits are immediate and substantial. For a full 15 years, you are exempt from two significant taxes:

- The 3% Property Transfer Tax: A one-time tax paid at closing on the property’s value.

- The 1% Annual Property Tax (IPI): A yearly tax on your real estate assets you won’t have to pay.

By eliminating these costs, you free up thousands of dollars. This capital can be used to increase your down payment, strengthening your offer and potentially lowering your interest rate. Alternatively, you can use it to furnish your new Caribbean home.

For a detailed breakdown, read our guide on investing in tax-free real estate with the CONFOTUR law.

This type of strategic saving is rare in other markets, especially for second homes. Most government incentives are for primary residents. For instance, California offers programs to help first-generation buyers, but these are not available to investors or international buyers. You can read more about California’s down payment assistance programs on sammamishmortgage.com.

Think of the CONFOTUR law as a government-backed subsidy for your investment. By removing major tax burdens right from the start, it allows you to begin earning a higher return from day one. It makes owning a premium Caribbean property far more accessible than most people think.

This is the on-the-ground, specialized knowledge that makes a difference. At Atlantique Sud, we don’t just find you a property; we uncover every financial advantage the Las Terrenas market offers to ensure your investment is as smart as it is stunning.

Building Your Las Terrenas Down Payment Fund

Planning your down payment is the first concrete step toward waking up to ocean breezes in Las Terrenas. This involves more than just saving; it requires a focused strategy to build your “paradise fund” efficiently. At Atlantique Sud, we provide real-world strategies designed for international real estate investment.

Start by setting up a dedicated savings account, separate from your everyday finances. A high-yield savings account is a great option, as it keeps your money accessible while allowing it to grow. This separation creates a clear mental and financial commitment to your goal.

Creating a Realistic Savings Timeline

A clear timeline transforms a dream into an achievable project. Work backwards from your goal. Let’s say you’re interested in a $350,000 beachfront condo—a popular choice with excellent rental income potential.

A typical 20% down payment would be $70,000. By setting aside $2,000 per month, you could reach that target in just under three years. A tangible roadmap like this makes the process feel manageable and keeps you motivated.

The challenge of saving for a down payment varies greatly by location. In a high-cost market like California, a household with a median income might need nearly 49 years to save a 20% down payment. You can learn more about how down payment sizes impact housing affordability on usmi.org. This highlights the accessibility of the Las Terrenas market for international buyers.

Your down payment fund is more than just money in an account; it’s your commitment to a new lifestyle. By being strategic and consistent, you can seriously speed up your timeline to owning a property in the Dominican Republic.

Accelerating Your Savings Growth

To reach your goal faster, consider investment vehicles with higher potential returns.

- Low-Cost Index Funds: These offer diversified exposure to the stock market and can significantly outperform a standard savings account over a few years.

- Systematic Investments: Consistency is key. Set up automatic monthly transfers to your investment accounts to leverage the power of compound growth.

- Leverage Existing Assets: A Home Equity Line of Credit (HELOC) on your primary residence can provide a lump sum for your down payment.

Building your down payment fund is the foundation of your investment journey. With a smart strategy and clear goals, you’ll be well on your way to securing your dream home on the Samaná Peninsula.

Frequently Asked Questions About Down Payments

As the most established real estate experts in Las Terrenas, we’ve guided hundreds of international buyers through this process. Here are answers to common questions about second home down payment requirements to give you clarity and confidence.

Can I use my home currency for the down payment?

While property prices are listed in US dollars, the down payment and final transaction must be made in USD. This is typically handled via a secure wire transfer to an escrow account managed by a reputable Dominican law firm. Our team at Atlantique Sud will guide you through this secure and straightforward process.

Is the down payment amount negotiable?

While the standard down payment percentage is usually firm, there can be some flexibility, especially with pre-construction projects where developers may offer structured payment plans. With our 25+ years of local experience, we leverage our network to negotiate the most favorable terms for our clients.

How are my down payment funds protected?

This is a critical question. The Dominican Republic has strong legal frameworks to protect buyers. Your down payment is held in a secure escrow account managed by your attorney, not the seller. Funds are released only when the legally binding conditions of your purchase agreement are met, ensuring transparency and security.

Your funds are protected through a legally mandated escrow process. The down payment is held in a secure account managed by your attorney, not the seller or developer directly. These funds are only released according to the legally binding terms of your purchase agreement, providing complete security and peace of mind throughout the transaction.

What is the timeline for purchasing a property?

For a resale property, the process from offer to closing typically takes 30-60 days. For pre-construction projects, the timeline depends on the construction schedule, which can range from 18 to 36 months, with payments structured around key milestones.

Your dream of owning a slice of paradise in the Caribbean is closer than you think. The expert team at Atlantique Sud Real Estate is ready to answer all your questions and guide you through every step, from understanding down payments to finding the perfect property.

Contact us today for a personalized consultation and discover the incredible opportunities waiting for you in Las Terrenas.