Rent to Own Dominican Republic: Your 2026 Guide

You’re probably looking at the Dominican Republic from a very practical angle. You like the lifestyle. You may already know Las Terrenas, or you’ve spent time in Punta Cana or Santo Domingo. But you don’t want to wire a full purchase price today, and local bank financing as a foreign buyer may feel slow, expensive, or unrealistic.

That’s where rent to own Dominican Republic deals start to make sense. Not because they’re easy, but because they can bridge a real gap between renting and buying when a standard mortgage isn’t the right fit. The problem is that many articles stop at a simple definition and skip the part that matters most: contract structure, title protection, tax treatment, and what happens if either side fails to perform.

A workable rent-to-own deal in the DR lives or dies on the paperwork. If the contract is vague, you’re not buying flexibility. You’re buying risk. If the property is clean, the purchase terms are locked properly, and your lawyer structures the agreement well, this can be a smart path for a foreign buyer who wants time, control, and a clearer route to ownership.

Table of Contents

- What Rent to Own Actually Means in the Dominican Republic

- The Anatomy of a Dominican Rent to Own Contract

- Evaluating the Pros and Cons for Foreign Buyers

- Key Risks and How to Mitigate Them

- Comparing Alternatives Seller Financing and Mortgages

- A Practical Due Diligence Checklist Before Signing

- Frequently Asked Questions About Rent to Own

What Rent to Own Actually Means in the Dominican Republic

A foreign buyer arrives in Las Terrenas after two or three scouting trips, finds a condo near Playa Bonita that fits the budget, but is not ready to wire the full purchase price or wait on a bank approval process that may drag. That is the situation where rent to own comes up in real conversations.

In the Dominican Republic, rent to own is a private agreement between buyer and seller that combines occupancy with a future purchase right. You move in under a lease-based arrangement, pay an agreed amount each month, and part of that payment may be credited toward the price if the contract says so clearly.

That last point matters more than many buyers expect. In the DR, “rent to own” is not one standard legal product with fixed rules. It is a negotiated structure. Some agreements are true lease-option contracts, where the tenant has the right, but not the obligation, to buy later. Others work more like a lease-purchase, where both sides are committing in advance to complete the sale if stated conditions are met. The practical difference is risk. A lease-option gives the buyer more flexibility. A lease-purchase usually gives the seller more certainty.

A simple example helps. The parties agree today on a sale price, a term, and how monthly payments are split. One portion covers use of the property. Another portion, if the contract provides for it, builds a credit ledger that is applied at closing. Title usually stays with the seller until the final sale deed is signed and recorded, so the buyer has possession without ownership. That is why I tell foreign clients to treat these deals as contract-driven transactions, not informal handshake arrangements with a real estate label attached.

This structure appeals to buyers who want time to live in the area before committing, especially in micro-markets where block-by-block differences matter. A unit that looks perfect online can feel very different once you have spent a few weeks there during high season, low season, rain, power outages, or heavy weekend traffic.

It also appeals to buyers who can afford the property but do not want all their cash tied up on day one, or who expect friction with local financing. In practice, many non-resident buyers use rent to own because it creates a path to control a property first and complete the purchase later, with terms negotiated directly with the owner rather than dictated by a bank.

For sellers, the attraction is straightforward. They keep rental income coming in, they may secure a future buyer at an agreed price, and they can set default terms that protect them if the tenant-buyer stops paying. Owners who care about tenant quality and presentation usually think about these deals much like premium rentals in the early stage. aiStager's guide to marketing rentals is a useful reference for how experienced landlords position a property before they ever discuss longer-term structures.

Foreign buyers should also understand what rent to own does not do. It does not transfer title early. It does not erase closing costs, transfer tax, or annual property tax exposure if the asset falls outside an exemption. It does not protect a buyer from title defects, liens, succession disputes, or condominium restrictions unless those issues are checked before signing. In the DR, the contract can create a path to ownership, but only careful drafting and due diligence make that path reliable.

A practical rule applies here. If the agreement does not state the purchase price or pricing formula, the credit amount, the treatment of missed payments, and what happens to credits if the deal ends early, you are looking at a rental with an option story attached, not a serious rent-to-own transaction.

The Anatomy of a Dominican Rent to Own Contract

A foreign buyer signs what looks like a simple lease, wires an upfront payment, moves into the villa, and starts planning around an eventual closing. Six months later, the seller tries to change the sale price, a title issue surfaces, and the buyer learns the contract never clearly said how rent credits would be applied. I have seen versions of this problem more than once in Las Terrenas. The document looked friendly. It was not built for a dispute.

A Dominican rent-to-own contract has to do two jobs at the same time. It must function as a lease during the occupancy period and as a sale framework that can close. If either side of that structure is weak, the buyer carries more risk than expected.

The five clauses that matter most

Start with the purchase right. The contract should say whether the buyer holds an option to purchase or whether both sides are already bound to complete the sale after stated conditions are met. That distinction matters. An option gives the buyer flexibility but usually comes with stricter timing and forfeiture rules. A lease-purchase model creates a firmer obligation, but sellers often resist it unless the default terms strongly protect them.

Next is the price clause. The best version is a fixed purchase price written into the agreement. If the parties use a formula instead, the formula has to be precise enough that no one is renegotiating later. “Market value at closing” is not precise. It invites conflict, especially in active areas where values can move quickly and each side can find a broker opinion that suits its position.

Then comes the payment allocation clause. Many weak contracts often fall apart at this point. The agreement should separate three figures clearly. Monthly rent, any nonrefundable option consideration, and the amount of each payment credited toward the purchase. It should also state whether credits reduce the final cash due at closing or are treated another way for accounting and tax purposes.

The fourth clause is default, cure, and forfeiture. A serious contract says what counts as default, how notice must be given, how long the buyer has to cure, and what happens to credits and deposits if the deal ends early. Foreign buyers should pay close attention here. Sellers often draft broad forfeiture language. Some of it is enforceable. Some of it is poorly written and creates room for litigation.

The fifth is possession, maintenance, and risk allocation. In the DR, I regularly see tenant-buyers taking on obligations that go far beyond a standard lease. Garden care and utility payments are normal. Structural repairs, latent defects, HOA special assessments, or major equipment replacement need to be assigned with precision. If the contract is vague, the practical result is simple. The party in a weaker position pays.

A good document also covers who pays transfer tax at closing, who pays notary and registration costs, and whether the seller must deliver the property free of liens and current on condominium fees. Buyers comparing this route with second home mortgage rates in the Dominican Republic should pay attention to that point. Rent-to-own can reduce bank dependence, but it often shifts more legal and drafting risk onto the buyer.

What good drafting looks like in practice

The contract should identify the property exactly as it appears in the title record, survey, and condominium documents if the asset is a unit. A street description is not enough. Unit number, parcel reference, certificate details, and boundaries all matter because a closing cannot be cleaner than the asset description in the agreement.

It should also restrict the seller’s actions during the contract term. If the seller can refinance the property, grant a mortgage, resell it, or transfer rights to an heir or third party without the buyer’s consent, the buyer’s path to closing is exposed. In practice, I want to see a clear prohibition on new encumbrances and a requirement that title remain transferable at closing.

The accounting section needs the same level of care. Every credited payment should be traceable in a ledger attached to the contract or updated under a written receipt procedure. If there is a later disagreement, a clean payment history matters as much as the legal language.

Foreign buyers should also separate the roles involved. The seller’s lawyer protects the seller. The notary legalizes signatures and formalities. Neither replaces independent counsel for the buyer. In a rent-to-own deal, that difference is expensive to learn late.

A well-drafted Dominican rent-to-own contract reads like it expects pressure. That is the right standard. Friendly deals stay friendly until money, title, taxes, or missed deadlines test them.

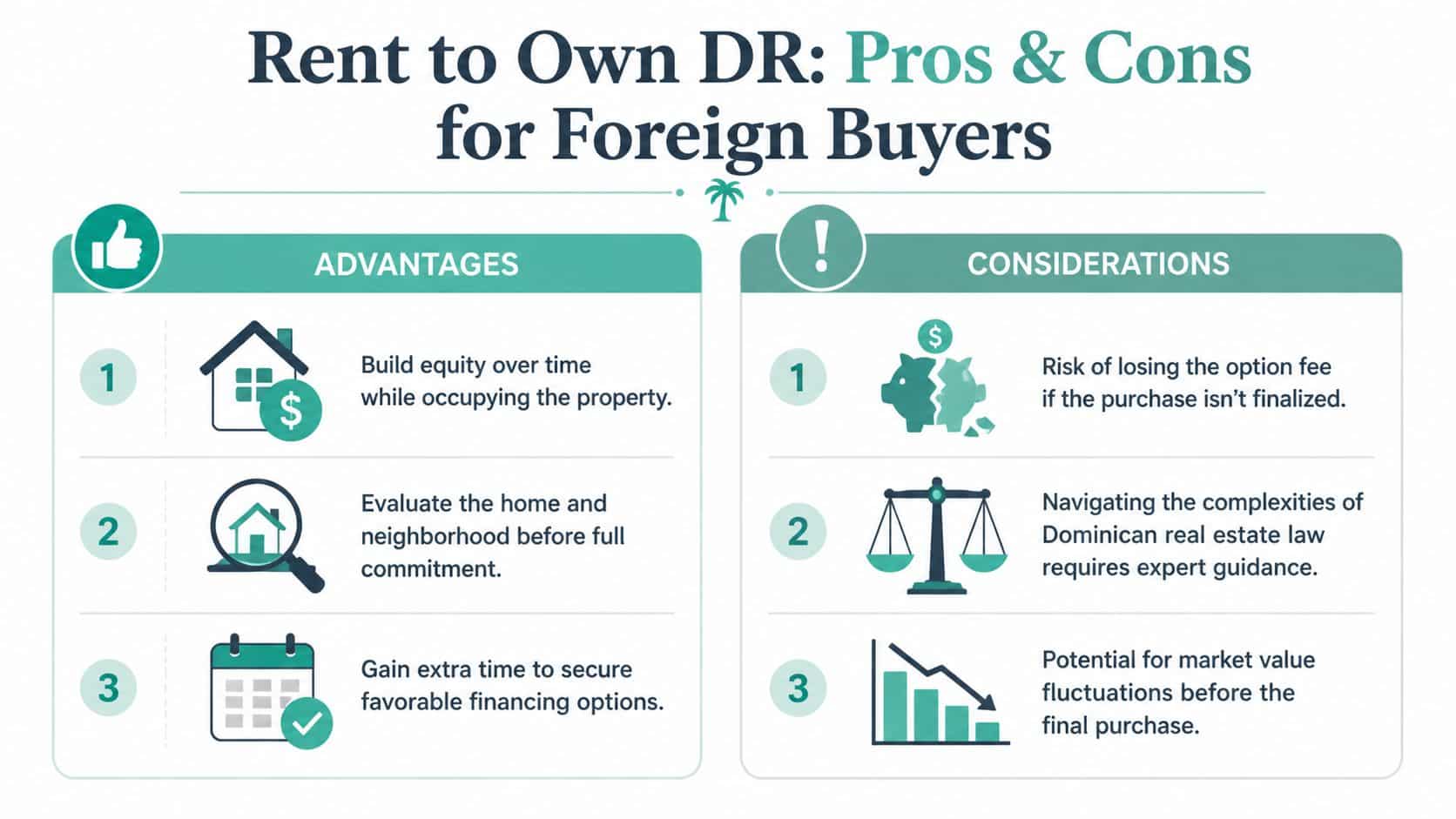

Evaluating the Pros and Cons for Foreign Buyers

Rent to own appeals to foreign buyers because it solves practical problems. It also creates a few new ones. The right way to judge it isn’t as “good” or “bad,” but as a set of trade-offs.

Where rent-to-own works well

The first advantage is time with purpose. You can live in or control the property while deciding whether that location really fits your life. That matters in micro-markets where the experience changes block by block. Cosón feels different from central Las Terrenas. Portillo feels different from El Limón. A lease-purchase structure gives you room to test the fit without losing sight of ownership.

The second advantage is equity-building while you wait. In a standard rental, the money is gone once paid. In a proper rent-to-own agreement, part of that payment moves you toward acquisition.

The third advantage is potentially lower management friction for absentee owners. Standard rentals often involve ongoing oversight, and property management fees typically range from 10% to 15% of monthly rent, while rent-to-own arrangements can create more stable, lower-turnover occupancy than short-term rentals, according to this discussion of Dominican income property management realities. That can matter if you live abroad and don’t want repeated tenant turnover.

One reason some buyers choose this route instead of immediate financing is the cost of conventional borrowing. If you want context on how second-home lending behaves more broadly, this article on second home mortgage rates helps frame the financing side of the decision.

Where it can disappoint buyers

The first drawback is you may tie up money without guaranteed title transfer. If the seller’s paperwork is weak, or the contract is sloppy, you can spend months or years paying into a structure that doesn’t protect you enough.

Another issue is limited flexibility once you’re committed. A buyer sometimes likes the concept more than the practical experience. Maybe the HOA is difficult. Maybe the traffic pattern near Pueblo de los Pescadores turns out to be noisier than expected. Maybe the building ages worse than you thought. Exiting early is usually more painful than leaving a plain lease.

Then there’s legal complexity. A standard rental dispute is one thing. A hybrid lease-purchase dispute is another. You’re dealing with possession, payment credits, default treatment, and future transfer rights at the same time.

A quick side-by-side view makes that easier to judge:

| Question | Rent to own | Standard rental |

|---|---|---|

| Do you build contractual purchase credit | Yes, if drafted clearly | No |

| Can you test the property before full purchase | Yes | Yes |

| Is the legal drafting more complex | Yes | Usually less |

| Is early exit usually simple | No | Often simpler |

| Does title transfer immediately | No | No |

Rent to own works best for buyers who are financially capable of buying, but not ready to buy immediately. It works poorly for buyers who hope the contract itself will fix a weak budget or unclear plan.

Key Risks and How to Mitigate Them

Most buyers focus on the visible risk. They ask whether they could lose the option fee or purchase credits. That’s important, but it isn’t the only danger.

The risks most buyers notice too late

The first hidden risk is seller-side trouble during the contract term. If the seller has financial problems, creditor issues, inheritance disputes, or title defects, your occupancy doesn’t automatically protect your future purchase rights. Buyers tend to discover this only when they try to close.

Title quality deserves special attention. If you want a plain-language overview of the kinds of issues that can surface in property records, Survey Merchant details property risks in a way that’s useful even outside the DR.

The second hidden risk is tax classification, a subject on which many public articles become too simplistic. A rent-to-own deal mixes rental payments and purchase credits, and investors need clarity on whether the “rent” portion is treated as rental income and how the “principal” portion is classified. That due diligence gap is specifically highlighted in this discussion of rent-to-own tax uncertainty in the Dominican Republic.

The third risk is default language that only protects one side. Some agreements are drafted as if every breach will come from the buyer. But sellers can default too. They can fail to maintain title, fail to deliver closing documents, or attempt to renegotiate if market values rise.

How to reduce those risks before signing

Strong prevention looks unglamorous. It’s mostly paperwork.

Use these protections:

- Add a no-encumbrance covenant: The seller should promise not to mortgage, transfer, or otherwise burden the property during the contract term.

- Require title monitoring: Your lawyer should check title status before signing and again before closing.

- Draft a detailed default section: It must cover buyer default and seller default, not just one.

- Get tax advice in writing: Your attorney and accountant should both review how payments will be documented and reported.

- Control the paper trail: Every payment should be traceable and matched to the contract’s allocation formula.

The safest rent-to-own agreement is the one that assumes disagreement in advance and still gives both sides a clear path to resolution.

Comparing Alternatives Seller Financing and Mortgages

A foreign buyer in Las Terrenas often reaches the same decision point. The property works, but paying all cash is too aggressive, and a standard bank loan may be slow, expensive, or out of reach as a non-resident. At that point, the true comparison is not just monthly payment size. It is how title transfers, who controls the default process, and how much legal risk sits with you before closing.

Three paths and what changes in practice

A mortgage is the cleanest structure on paper. The sale closes, title transfers, and the bank records its security. If you want a plain-English primer on how loan structures work, EHF Mortgages home loan advice is a useful starting point. In the Dominican Republic, though, foreign buyers should expect more friction than they would in the US, Canada, or Europe. Banks often want extensive income documentation, local account history, and a larger down payment than buyers first expect.

Seller financing usually gives more room to negotiate. The buyer and seller agree on price, down payment, interest, term, default remedies, and when title transfers. In some deals, title transfers at closing with a mortgage or vendor lien recorded in favor of the seller. In others, the seller keeps title until the final payment. That difference matters. A seller-financed sale can be cleaner than rent to own because it starts as a purchase transaction, but only if the documents are drafted with the same discipline you would expect from a bank. This guide to what seller financing is in real estate explains the core structure well.

Rent to own sits in the middle. It can reduce upfront pressure and give a buyer time to test the property, the area, and the timing of a later purchase. It also creates more room for dispute because part of the relationship looks like a lease and part looks like a future sale. That hybrid structure is exactly why I treat rent to own as the most document-sensitive option of the three.

Here is the practical comparison:

| Factor | Rent to own | Seller financing | Bank mortgage |

|---|---|---|---|

| Upfront cash pressure | Often lower than a full purchase | Negotiable with seller | Usually higher |

| Qualification friction | Moderate, contract-driven | Depends on seller’s standards | Usually highest |

| Title transfer timing | Later, after option exercise or final condition | Depends on contract structure | At closing |

| Default handling | Can become messy if lease and purchase terms conflict | Negotiable, but must be drafted carefully | More standardized |

| Tax treatment | Often less clear | Usually easier to document as a sale | More predictable |

| Best use case | You want time before committing to close | You want installment buying with purchase terms set now | You qualify and want immediate ownership |

The better option depends on what risk you can tolerate

Choose a mortgage if you qualify and want the clearest path to ownership. The bank will be demanding, but the structure is familiar, title usually transfers right away, and there is less ambiguity about whether you are a tenant or an owner.

Choose seller financing if the seller is credible, the title is clean, and both sides are ready to structure the deal as a real sale from day one. In practice, this is often the strongest alternative for foreign buyers who cannot or do not want to depend on a Dominican bank.

Choose rent to own if time has value to you. That may mean verifying the neighborhood through one full high season and low season, staging funds from abroad, or waiting for residency, business income history, or a sale in your home country. The trade-off is legal complexity. You need tighter drafting, clearer payment allocation, and stronger protections if the seller fails to perform.

The short version is simple. Mortgages are more rigid but cleaner. Seller financing is flexible and can be efficient. Rent to own offers breathing room, but it only works well when the contract closes the gaps that foreign buyers usually do not see until a dispute starts.

A Practical Due Diligence Checklist Before Signing

A rent-to-own deal should never begin with enthusiasm. It should begin with verification.

The pre-signing checks that are not optional

Use this as your pre-signing checklist:

Confirm the seller’s identity and authority

Make sure the person signing owns the property or has the legal power to sell it. If a company owns the asset, verify who can bind that company.Verify the title status and survey situation

You want clean title, and you want the property properly identified. In practical DR terms, buyers should pay close attention to whether the asset has proper surveyed boundaries and title clarity. This broader real estate due diligence checklist is a useful reference point.Check for liens, disputes, or restrictions

Don’t assume that because a property is occupied or marketed, it’s free of legal baggage. Your lawyer should review the title history and current status independently.Inspect the physical property

A rent-to-own buyer sometimes accepts maintenance obligations earlier than a standard tenant would. That makes condition more important, not less. A building problem discovered after signing can become your problem very quickly.Review condo rules and common charges

In Las Terrenas, this matters especially in condominium communities near Playa Bonita, Portillo, and central beach zones. Building rules can affect occupancy, use, repairs, and even eventual rental strategy.Have an independent attorney draft or revise the agreement

This is not a form-download situation. Your lawyer should review the lease terms, purchase option, default language, title protections, and closing mechanics as one integrated transaction.Clarify tax handling before the first payment

Don’t wait until year-end to ask how the payment streams should be treated. The contract language and accounting treatment should align from day one.

A clean property can still be a bad rent-to-own deal. A well-located condo in Playa Bonita is not automatically safe if the contract is weak.

Frequently Asked Questions About Rent to Own

Can I leave the deal early

Usually yes, but the contract decides the cost of that exit. Some agreements are strict and treat early departure as buyer default. Others allow negotiated termination. What matters is whether your credits are forfeited, partially returned, or applied in some other way.

Can the seller change terms during the lease

Not if the agreement is drafted properly. The contract should lock the key commercial terms, especially the purchase price, timing, and credit treatment. If those points are left vague, the seller may try to reopen the conversation later.

Does CONFOTUR automatically carry over to a rent-to-own deal

No buyer should assume that. Tax incentives may exist for qualifying tourism properties, but whether they apply, how they apply, and whether anything changes during a lease-purchase period should be confirmed with your attorney and accountant on the specific property.

Are these deals common in Las Terrenas

They exist, but they’re still a niche structure. You’ll see them more often when a seller wants to widen the buyer pool, when a foreign buyer needs time before closing, or when both sides are trying to avoid the friction of conventional financing.

The key point is simple. A rent-to-own arrangement can be useful in Las Terrenas, Playa Bonita, Cosón, Portillo, or El Limón, but only when the property is clean and the contract is unusually precise. This isn’t the place for handshake logic.

If you’re weighing a rent to own Dominican Republic deal and want a clear view of the legal, title, and financing trade-offs before you commit, contact Atlantique Sud Real Estate for a personalized market consultation.