Calculating Cap Rate on Rental Property: A 2026 Investor’s Guide

When you're evaluating rental properties in Las Terrenas, how do you cut through the hype and compare them fairly? You use the capitalization rate. The cap rate is a straightforward formula that shows a property's annual return on investment, independent of financing. It’s the single most important number for comparing one opportunity to another, as it reveals a property's raw earning potential.

For investors looking at Las Terrenas, this isn't just theory—it's how you decide between a villa in Playa Bonita and a condo in the Pueblo de los Pescadores with total confidence.

Table of Contents

- What Is Cap Rate and Why It Matters for Las Terrenas Investors

- How to Calculate Your Net Operating Income Accurately

- A Real-World Las Terrenas Cap Rate Calculation

- Common Cap Rate Mistakes We See Investors Make

- How to Interpret Your Cap Rate in the Dominican Republic

- Your Cap Rate Questions Answered

What Is Cap Rate and Why It Matters for Las Terrenas Investors

Think of the cap rate as an investment's vital sign. It provides a standardized way to measure potential returns, allowing you to compare a beachfront home in Cosón with a new development in Portillo on an apples-to-apples basis. As local market experts with over 25 years of experience, we use this metric every single day to vet opportunities for our clients.

This isn’t some textbook definition; it's a practical tool we use to get to the facts. Understanding this metric is the first step toward thinking like a seasoned investor, not just a homebuyer. Acknowledging this is crucial because it protects you from overpaying or choosing an underperforming asset.

The Core Concept

A cap rate is simply a property's Net Operating Income (NOI) divided by its current market value or purchase price. The result is a percentage that quickly shows you its profitability. If you want to go a bit deeper, check out this excellent Top Wealth Guide's cap rate guide.

A cap rate directly links a property's annual income to its price. For example, a property that generates $42,000 of net operating income on a $600,000 value has a 7% cap rate. This means every $100,000 of its value needs to produce $7,000 in annual NOI to hit that target.

This simple calculation is powerful because it focuses on net income, not just gross rent. You have to subtract all the operating expenses—like taxes, insurance, and management fees—to get a true picture of performance. We’ve actually written a more detailed article if you're curious about what a cap rate is in real estate investing.

Las Terrenas Cap Rate at a Glance

To give you a quick lay of the land, here are some typical cap rate ranges you'll find in the Las Terrenas market. Our current market data shows rental yields from 5.6% to 7.7%, but well-managed properties can perform even better. Use this as a benchmark to see how a potential investment stacks up.

| Investment Type | Typical Cap Rate Range | Risk & Effort Profile |

|---|---|---|

| Luxury Beachfront Villa | 4% – 6% | Lower Risk, Lower Effort (with management) |

| Downtown Condo (Long-Term Rental) | 6% – 8% | Moderate Risk, Moderate Effort |

| New Development (CONFOTUR) | 7% – 9% | Moderate Risk, Low Initial Effort |

| Short-Term Rental (Airbnb) | 8% – 12%+ | Higher Risk, Higher Effort (active management) |

Remember, these are just general guidelines. A property's specific location, condition, and management will always play a huge role in its final performance.

Interpreting Risk and Reward

Different cap rates tell a story about risk and potential reward. In any market, you'll see this relationship play out:

Lower Cap Rates (e.g., 4-6%): These often signal a stable, lower-risk asset in a highly desirable, mature location. Think of a prime villa on Playa Bonita. They are considered safer bets but with more modest cash flow.

Higher Cap Rates (e.g., 9-12%+): These can point to higher potential returns but may come with more risk or require more hands-on work. This might be a property in an up-and-coming area like El Limón or a rental that needs very active management to hit its numbers.

In a dynamic, high-growth market like Las Terrenas, understanding this balance is absolutely vital. Our market consistently offers yields that are far more attractive than what you'd find in most established North American or European cities, making it a fantastic place to put your capital to work.

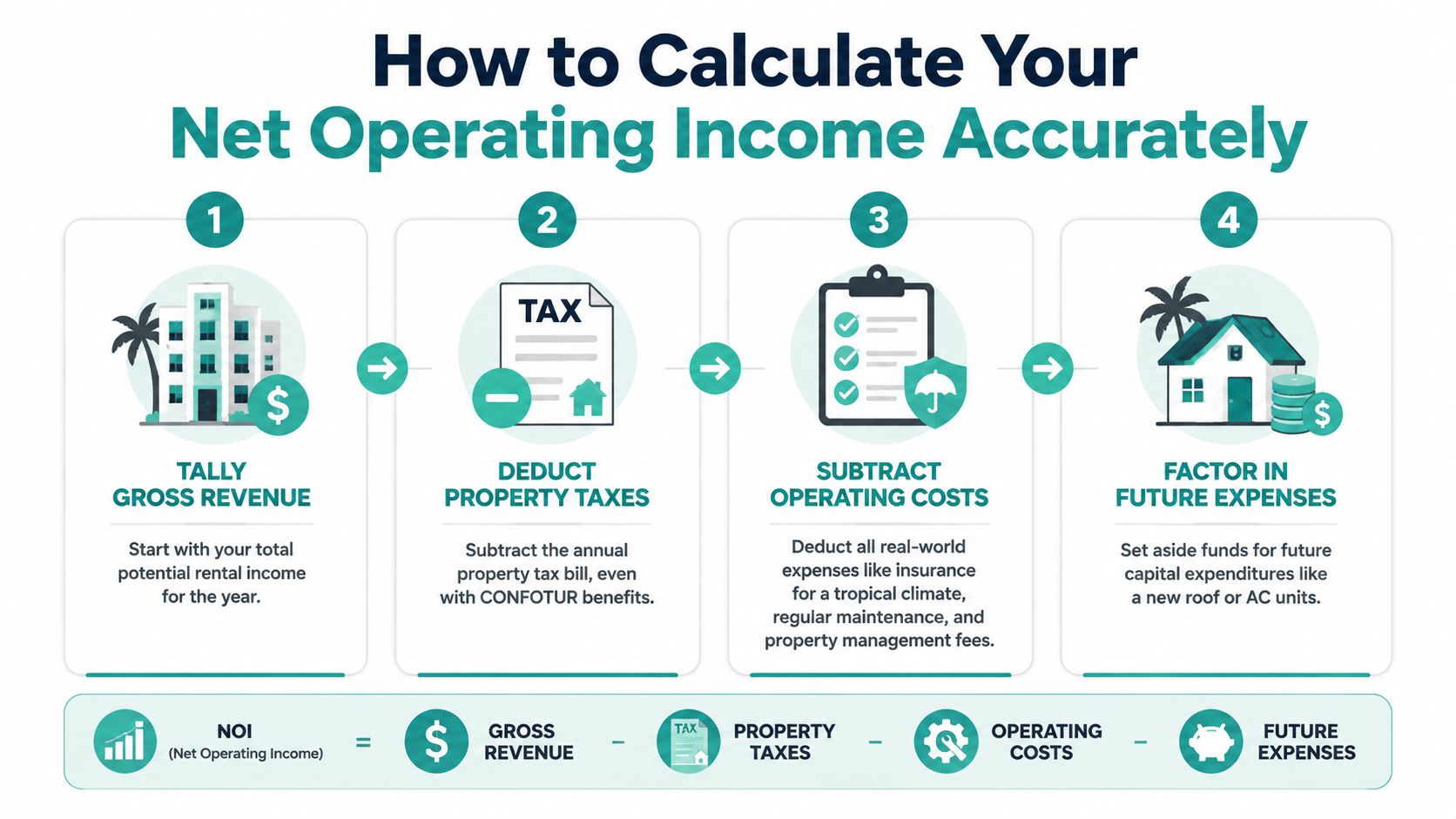

How to Calculate Your Net Operating Income Accurately

If there’s one place where investors trip up—new and seasoned alike—it’s right here. Your Net Operating Income (NOI) isn't just your rental income minus a few bills. Getting this calculation right is the absolute bedrock of figuring out a realistic cap rate for a property in Las Terrenas.

A rosy, overly optimistic NOI will give you an inflated cap rate and set you up for major disappointment. You have to get real about all the operating expenses that will inevitably eat away at your revenue. This is about more than just subtracting a generic percentage; it's about digging into the true costs.

Key Expenses to Deduct

To get to a real-world NOI, you’ll start with your gross potential rental income and then subtract all the annual costs of running the property. Here are the non-negotiable expenses you must factor in:

- Property Taxes: Don't assume a property is tax-free. Even if it qualifies under CONFOTUR, which grants a 15-year exemption on the 1% annual property tax, you need to verify its current status. If that benefit doesn't apply or has run its course, this is a real annual cost.

- Insurance: A generic policy simply won't do here. You need specific coverage for a tropical climate, which absolutely must include clauses for hurricanes and for the property being used as a rental business.

- Property Management Fees: For most of our clients investing from abroad, professional management isn't a luxury—it's essential. In Las Terrenas, these fees typically run from 10% to 20% of your gross rental income, depending on the level of service you need.

- Maintenance and Repairs: The tropical environment is beautiful, but the sun, humidity, and salt in the air are relentless on a building. A dedicated maintenance budget is crucial. Using a detailed ultimate property upkeep checklist can be a lifesaver to make sure you're not missing anything.

- HOA Fees (Condo Fees): If you're looking at a condo or a villa inside a gated community, you'll have monthly fees. These cover shared amenities like pools, security, and landscaping, and they can be a significant recurring expense.

Crucial Reminder: Your mortgage payment (principal and interest) is never included when calculating NOI. NOI is all about the property's ability to generate profit before debt. The return you see in your pocket after your loan payments is called cash-on-cash return. You can learn more about the difference in our guide on how to calculate real estate ROI.

Don't Forget Future Capital Expenditures

One of the most common and costly mistakes we see is investors failing to budget for large, infrequent expenses, known as Capital Expenditures (CapEx). These aren't your monthly maintenance bills; they are the big-ticket items you know will eventually need replacing.

Think of it as a mandatory savings account for your property's future. This fund covers things like replacing a roof, putting in new AC units, or updating all the major appliances.

A solid rule of thumb is to set aside 5% to 10% of your gross rental income every single year into a separate reserve fund just for CapEx. Ignoring this will give you a dangerously false sense of profitability and an inaccurate cap rate.

A Real-World Las Terrenas Cap Rate Calculation

Theory is one thing, but let's get our hands dirty with some real numbers from right here in the Dominican Republic. To show you exactly how we analyze properties at Atlantique Sud, we’ll walk through two detailed case studies using USD: one for a steady long-term rental and another for a high-demand short-term vacation villa.

This whole process, which you can see in the infographic below, is all about getting from your property's gross income to its Net Operating Income (NOI). That's the magic number.

As you can see, accurately calculating the cap rate on a rental property demands that you subtract all the real-world expenses, not just the ones that jump to mind first. This kind of discipline is what keeps your investment projections grounded in reality and prevents nasty surprises down the road.

Case Study 1: The Long-Term Rental Condo

Let's start with a classic scenario: a two-bedroom condo in a great central Las Terrenas spot, valued at $280,000. It’s consistently rented out to an expat for $1,500 per month.

- Gross Annual Income: $1,500 x 12 = $18,000

- Vacancy Allowance (5%): -$900

- Effective Gross Income: $17,100

Now, we have to account for the real costs of owning and operating the property:

- HOA Fees: -$2,400/year ($200/month)

- Insurance & Taxes: -$1,800/year

- Maintenance Fund (5% of EGI): -$855

- Property Management (10% of EGI): -$1,710

Total Operating Expenses: $6,765

That leaves us with a Net Operating Income (NOI) of $10,335. So, we take that NOI and divide it by the property's value: $10,335 ÷ $280,000. The result is a cap rate of 3.7%. This is a typical return for a stable, lower-effort investment like a long-term rental.

Case Study 2: The Short-Term Vacation Villa

Now for something a little different. Let’s look at a three-bedroom villa near the beautiful Playa Bonita, valued at $500,000. This property pulls in an average of $350 per night.

For a vacation rental, the math starts with nightly rates and, crucially, occupancy. We'll project a realistic 75% occupancy based on what we’re seeing in the Las Terrenas market right now. This is where excellent management really shows its worth—even a small dip in bookings can drastically change your returns. If you want to go deeper into this dynamic, Guesty.com has a great breakdown on vacation rental cap rates.

- Gross Annual Income: $350 x (365 days x 0.75) = $95,812

As you’d expect, the running costs for a short-term rental are quite a bit higher:

- Management & Booking Fees (20%): -$19,162

- Utilities, Cleaning & Supplies: -$12,000/year

- Insurance & Taxes: -$3,500/year

- Maintenance Fund (7% of EGI): -$6,706

Total Operating Expenses: $41,368

That gives us an NOI of $54,444. Running the formula one more time ($54,444 ÷ $500,000), we land on a cap rate of 10.9%. That much higher return is the reward for taking on more management effort and the risks that come with seasonality.

Common Cap Rate Mistakes We See Investors Make

With over 25 years in the Las Terrenas real estate market, we've seen it all. This includes watching smart investors make the same preventable mistakes over and over.

An inflated cap rate might look impressive on paper, but it leads to serious disappointment when reality hits. This is our honest advice, from one professional to another, to protect you from those costly errors.

Let's start with the most common trap: taking a seller's pro-forma numbers at face value. These are almost always best-case-scenario projections that assume things like 100% occupancy and rock-bottom expenses—two things that simply don't exist in the real world. It's on you, the buyer, to independently verify every income and expense figure.

Overlooking True Costs and Vacancy

Another frequent misstep is not factoring in a realistic vacancy rate. No property, not even a stunning villa right on Playa Cosón, is booked every single night of the year. Forgetting to budget for those empty nights will give you a dangerously optimistic cap rate.

On that same note, so many investors either ignore or seriously underestimate future capital expenditures (CapEx). That fund for a new roof, updated AC units, or resurfacing the pool isn't just an "extra." It's a real, predictable cost of owning property that has to be baked into your numbers from day one.

A complete cap rate analysis should always reflect the true acquisition cost, not just the sticker price. This includes all closing costs, legal fees, and transfer taxes, as these expenses directly impact your real return on capital.

Using the Wrong Denominator

Finally, a critical error we see is using the property's list price in the cap rate formula instead of its total acquisition cost. Here in the Dominican Republic, your total cost will always include transfer taxes and legal fees, which can add a significant chunk to the purchase price.

Using only the list price will artificially inflate your cap rate and set you up for a fall. If you're interested in a deeper dive, you can learn more about how professionals use cap rates for valuation at this in-depth resource from Mynd.co.

By sidestepping these common pitfalls, you ensure your investment decisions are built on a solid, realistic foundation—not just wishful thinking.

How to Interpret Your Cap Rate in the Dominican Republic

So, you've run the numbers and have a cap rate. Great! But a cap rate is just a number until you put it into the context of the local market. Knowing how to read that figure within the unique real estate landscape of the Dominican Republic is what separates a casual buyer from a smart investor.

Here in Las Terrenas, we’re seeing average rental yields typically fall somewhere between 5.6% to 7.7%. That said, for a well-managed short-term vacation rental, it's very possible to see returns in the 8% to 10% range, and sometimes even higher. This easily outshines many other Caribbean hotspots like Tulum, where sky-high property prices can really squeeze your yields.

What Is a "Good" Cap Rate Here?

Honestly, a "good" cap rate really hinges on your personal goals and how much risk you're comfortable with. A lower cap rate might be perfectly fine for a turnkey villa in a prime, established area like Playa Bonita. In that case, you're not just buying cash flow; you're also betting on strong, long-term appreciation.

On the other hand, a higher cap rate is often found in up-and-coming neighborhoods like Portillo or El Limón. That bigger number is your reward for taking on a bit more perceived risk, or for a property that needs more hands-on management to hit its full earning potential.

Cap Rate vs. Cash-on-Cash Return

It is absolutely vital to understand the difference between cap rate and your personal return. A cap rate shows you a property's performance without any financing—it’s the raw, unleveraged return. Your Cash-on-Cash Return, however, measures the return on the actual cash you’ve put into the deal, after factoring in your mortgage payments.

Using financing dramatically changes your personal returns. A property with a 7% cap rate could easily generate a 15% or higher cash-on-cash return depending on your loan terms. This is a key part of any savvy investor's strategy.

Ultimately, interpreting a cap rate means understanding the story it tells about the property and its specific sub-market. If you’re digging deeper into the financial side of your investment, you can learn more about the Dominican Republic's tax system in our guide.

Your Cap Rate Questions Answered

When you get serious about buying a rental property, the theory quickly gives way to practical questions. We get it. As boots-on-the-ground experts in Las Terrenas, we’ve guided countless investors through the numbers.

Here are the most common—and most important—questions we hear about calculating the cap rate on a rental property, along with our straight-to-the-point answers.

What Is a Good Cap Rate for a Vacation Rental in Las Terrenas?

For a short-term vacation rental here, you'll want to see a cap rate in the 8% to 12% range. That’s the sweet spot.

This is naturally higher than what you’d expect from a long-term rental, and for good reason. It reflects the more hands-on management, the swings of seasonality, and the higher running costs that come with the vacation market. If a property is showing a cap rate below 8%, it might be a signal that it's overpriced for its earning potential. On the flip side, anything above 12% could be a fantastic deal—but it also warrants a closer look to make sure there aren't any hidden issues.

How Do CONFOTUR Tax Incentives Affect My Cap Rate Calculation?

This is a huge one. The CONFOTUR tax exemption rewrites your numbers. By wiping out the 1% annual property tax for 15 years, it directly boosts your Net Operating Income (NOI).

A bigger NOI, divided by the same purchase price, means a higher cap rate. Simple as that. It’s a powerful government incentive that makes qualifying new developments especially appealing from a pure return-on-investment perspective.

Should I Use the Asking Price or Total Purchase Cost to Calculate Cap Rate?

Always, always use your total purchase cost. This is a rookie mistake we see people make, and it can paint a dangerously rosy picture.

Your true investment isn't just the sticker price. The denominator in your cap rate formula must include the property’s price plus all your closing costs. That means things like the 3% transfer tax (if it applies) and your legal fees. Using only the asking price will give you a falsely inflated cap rate and an inaccurate projection of your actual return.

Can I Calculate a Cap Rate for a Pre-Construction Property?

Yes, and you absolutely should. This is what we call a pro-forma cap rate, and it’s a vital piece of your due diligence.

You'll start with the developer's projected rental income and estimated expenses. But—and this is critical—you need to stress-test those figures. Compare them against current market data for similar finished properties. Plug in realistic vacancy rates. A pro-forma cap rate is an essential tool for gauging the true potential of an off-plan investment before you put any money down.

Want to run these numbers on a real listing? Our Las Terrenas ROI Calculator computes cap rate, NOI and cash-on-cash return automatically — just enter the purchase price and nightly rate.

Contact Atlantique Sud for a personalized market consultation. We can walk you through a detailed cap rate analysis on any property you're considering.